Best Debt Consolidation Solutions to Buy in July 2026

DEBT CONSOLIDATION: How To Manage Debt And Become Debt Consolidation Expert

The Debt Consolidation Myth: A Proven Method to Help You Get Out of Debt While Still Living Your Life (YNAB 80/20 Book 2)

How to Deal with Debt Collectors and Win Every Time How To Beat Them at Their Own Game: YOUR NUMBER ONE GUIDE TO BEATING DEBT COLLECTORS

Debt 101: From Interest Rates and Credit Scores to Student Loans and Debt Payoff Strategies, an Essential Primer on Managing Debt (Adams 101 Series)

How to Be Debt Free: A simple plan for paying off debt: car loans, student loan repayment, credit card debt, mortgages and more. Debt-free living is within ... Finance Books) (Smart Money Blueprint)

BACK TO THE BASICS: Debt consolidation and basic real estate knowledge and investment

Debt Relief Success: How To Use Debt Relief To Gain Financial Freedom

How to get out of debt: the quick, simple, easy to understand guide to your financial freedom: credit card debt, debt free, debt consolidation, debt help, debt review, increase income, lower expenses

Debt Survival Guide: Managing Debt and Credit in Hard Times (Financial Survival)

JPMorgan’s Fall and Revival: How the Wave of Consolidation Changed America’s Premier Bank

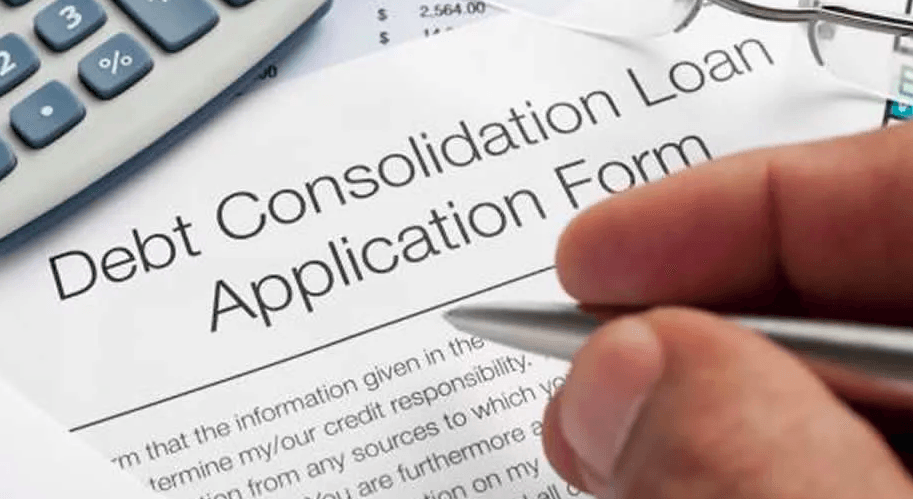

If you’re in over your head in debt, you may wonder how to find the best way to consolidate debt. Making minimum payments gets you nowhere, but you can’t afford anything else. If you’re tired of living under the burden of debt, consider a debt consolidation loan.

Debt consolidation loans aren’t hard to get. They can help you financially, and may even improve your credit score.

Check out the best debt consolidation companies below.

What is a Debt Consolidation Loan?

A debt consolidation loan is typically an unsecured loan you take out with a personal loan lender without putting down any collateral.

Unlike a mortgage or car loan, personal loan lenders don’t have anything to fall back on if you default. In exchange for the ‘flexible guidelines’ they charge higher interest rates and/or more fees, but they are often much less than you’d pay on your high interest credit card debt and are one of the best ways to consolidate debt.

Today, the average personal loan interest rate is around 9.5% and the average credit card interest rate is just under 16%, so it’s easy to see how a debt consolidation loan can help.

But how do you get one?

How to Apply for a Debt Consolidation Loan

Most companies offer debt consolidation loan applications online. It takes just a few minutes with the following steps:

- Complete a loan application. You’ll answer questions about yourself, income, and assets. Make sure you know how much money you need (the total of your debts) too.

- You’ll receive an offer(s) from one or more lenders. Compare the offers provided to determine which loan suits you the most. Look at the interest rate, fees, and cost of the loan over its lifetime.

- Choose an offer and let the lender pull your credit. Once you are ready to move forward, the lender will do a hard pull on your credit report to make sure you qualify.

- Provide any necessary documentation. Lenders may ask for your paystubs, W-2s, tax returns, or bank statements.

- Receive the funds. Usually, you’ll receive funds within one to five business days depending on the chosen lender.

How do Debt Consolidation Loans Work?

When lenders fund the loan, they direct deposit the funds in your bank account. You then use the funds as needed. In other words, you are in charge of paying your creditors off. Make sure you have your statements ready and know exactly how much to send to each creditor.

Now, rather than multiple payments each month, you make one payment to your personal loan lender. It helps keep you organized (no more missed payments). Plus, debt consolidation loans typically have lower interest rates than you pay on your credit cards, making it one of the best ways to consolidate debt.

How much can I Borrow?

Like any other loan, the amount you can borrow varies based on your qualifications and/or needs. Debt consolidation lenders usually offer loans from $1,000 to $50,000. The more money you need, the higher qualifications you need.

Can you get a Debt Consolidation Loan with Bad Credit?

Personal loan lenders consider ‘bad’ credit anything less than 630 in most cases. This doesn’t mean you can’t get a debt consolidation loan with bad credit, but you may pay higher interest rates or fees.

If you have bad credit do one of the following:

- Look for a personal loan lender who allows cosigners. Not all lenders do, so read the fine print. If you have a cosigner with good credit who’s willing to go on the loan, you increase your chances of approval and/or getting lower rates.

- Work on your credit. If you know the issues with your credit, work on it. Bring your late payments current, fix any errors, or report any fraudulent information to the credit bureaus right away.

If you can’t fix your credit or are in a hurry, look for one of the best debt consolidation loans for bad credit. Just watch the terms to make sure you aren’t paying more than you already do on your current debt.

Do Debt Consolidation Loans Hurt your Credit?

Initially, you may see a drop in your credit score, when you take out a debt consolidation loan. That’s only because you increased your outstanding credit. If you pay your credit cards off right away, though, your credit score will likely increase rather quickly.

The second largest component of your credit score is your credit utilization or a comparison of your outstanding credit compared to your total credit line. Once you pay your credit cards off in full, your credit score will reflect the lower credit utilization.

What is a Good Debt Consolidation Loan APR?

Debt consolidation loan APRS average around 10%, but can go as high as 35.99% depending on the lender and your qualifications.

Compare the APR offered to you to the interest rates you pay on your credit cards or other consumer debt. Is there a savings? Look not only at the monthly payment (it may be higher than individual debts if you consolidate debt) but at the cost of the loan over its term. Compare it to the total cost of your individual debts.

If you can save money, it’s worth consolidating your debt and improving your credit score.

Can you Pay off a Debt Consolidation Loan Early?

Most lenders don’t charge prepayment penalties but read the fine print. You can usually pay the loans off early, saving you even more money on interest. If you have extra money, after making the minimum required payment, pay your principal balance down and get out of debt faster.

Look for the Best Debt Consolidation Companies to Save the Most Money

The purpose of a debt consolidation loan is to save money, not only monthly, but over the life of the debt. Look for the best debt consolidation companies for the most attractive terms, lowest rates, and most flexible underwriting guidelines.

If you’re tired of living under the burden of excessive consumer debt, it’s time to consolidate and get your finances back on track. Lock up your credit cards and pay your balances off so you improve your credit score and achieve the financial freedom you desire.